‘Budget 101’: How KPBSD organizes funds

Published 10:30 pm Tuesday, December 12, 2023

How the Kenai Peninsula Borough School District organizes the money it gets and spends was the subject of the final installment in the district’s informational “Budget 101” series, which Finance Director Elizabeth Hayes delivered to school board members during a Dec. 4 work session.

Hayes kicked off the presentation, which was billed as an explanation of the district’s Chart of Accounts, by talking about the nomenclature the district uses to identify different pieces of their budget items, called account codes.

There are thousands of account codes used by the district in its budget, Hayes said, but each piece of the code indicates a specific fund, function, object, school site or program. Account codes are found on documents like expense reports as well as in the district’s annual budget.

“All of our data in the finance system is going to have some type of an account code structure assigned to it,” Hayes said.

The five pieces described by one account code include:

A three-digit number that says which district fund is affected;

A two-digit number that says which school is affected;

A four-digit number that says whether the account functions as a source of revenue or as an expenditure;

A four-digit number that says which program is affected; and

A four-digit number that most discretely describes a source of revenue or an expenditure.

Hayes gave 100-07-4100-0600-3150 as an example of one account code. From left to right, the pieces of the code indicate that the account impacts the KPBSD General Fund (100), corresponds to Kenai Central High School (07) and covers, as part of regular instruction (4100), science (0600) teachers (3150).

When looking at the district’s expenditures by function for the current fiscal year, which Hayes presented as a pie chart, more than half — 58.8% — of KPBSD’s roughly $141 million in expenditures went to some type of school instruction. Another 15% went to school or district administration and support for administration.

Hayes said “district administration” covers the school board, the superintendent and the assistant superintendent, while “administration support” includes directors.

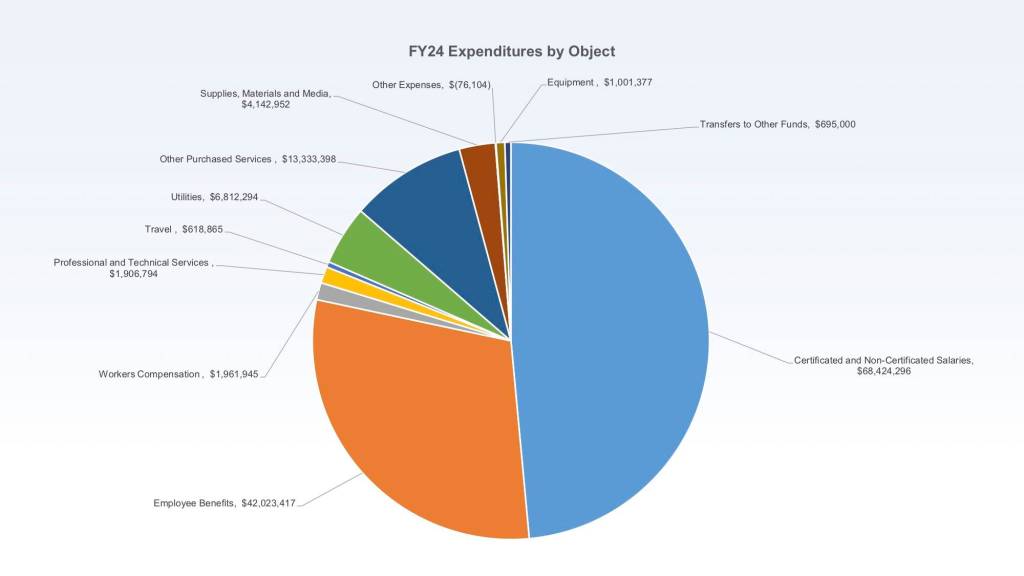

Looking at the district’s expenditures by object, rather than by function, Hayes showed that 79.8% of all KPBSD expenditures went to salaries for certified and non-certified staff members, to employee benefits and to workers compensation. The next largest pie slice is “other purchased services,” at $13.3 million, which Hayes said reflects in-kind services provided by the borough.

“There’s not a lot of areas other than salaries and benefits that we have a lot of wiggle room in,” Hayes said.

It’s possible that the proportion of district expenditures going to staff salaries and benefits goes up for the next fiscal year, Hayes said, even if the district keeps the same number of employees it has currently. That’s because the district is currently funding 66 positions — 60 certified and six non-certified — with federal COVID-19 relief funds, which the district no longer has.

KPBSD School Board President Zen Kelly said salaries and benefits previously accounted for about 86% of all district expenditures.

Hayes’ presentation marked the last in the district’s “Budget 101” series, which was announced in August as a way to inform the general public about how KPBSD’s budget process works. Previous installments in that series can be streamed on the district’s BoardDocs page.

Reach reporter Ashlyn O’Hara at ashlyn.ohara@peninsulaclarion.com.